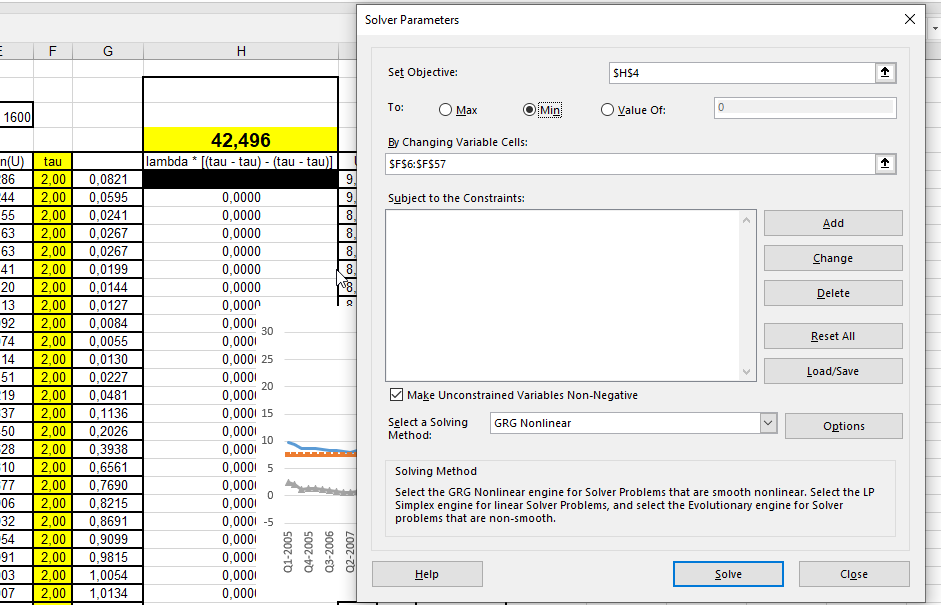

In excel, the infamous “excel solver” does the job to minimize the penalty function for me. In KNIME, I think the optimization loops can be helpful, however, I am stuck here.

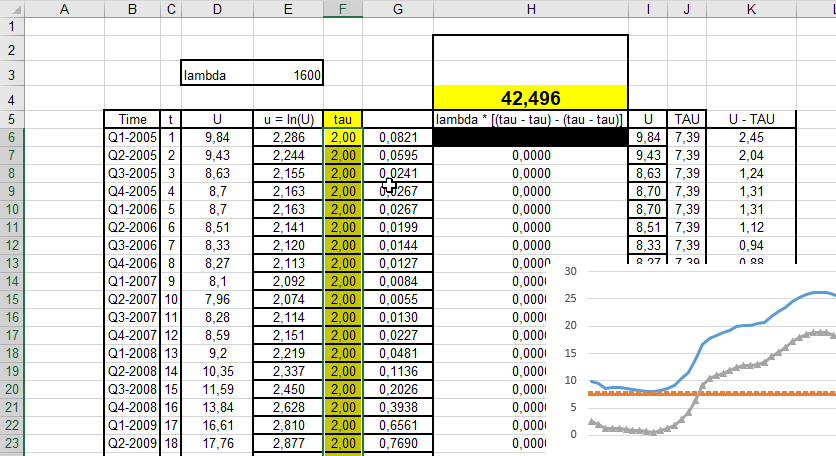

Data looks like this:

In cell H4, we have the function which should be minimized. It is a function of values that are available and one random variable (tau), which is found in column F. “tau” has a dummy value here of 2 for now, which needs to be optimized to minimize the penalty.

How would be the solution in KNIME? Any similar functionality to the excel solver? I have a feeling that one would need recursive loops and optimization loops here, but this sounds scary tbh.

Thanks for the reply!

I had a look at the GA node, however, I am not too familiar with it. But I think it is definetly worth looking more into it for future, similar, problems.

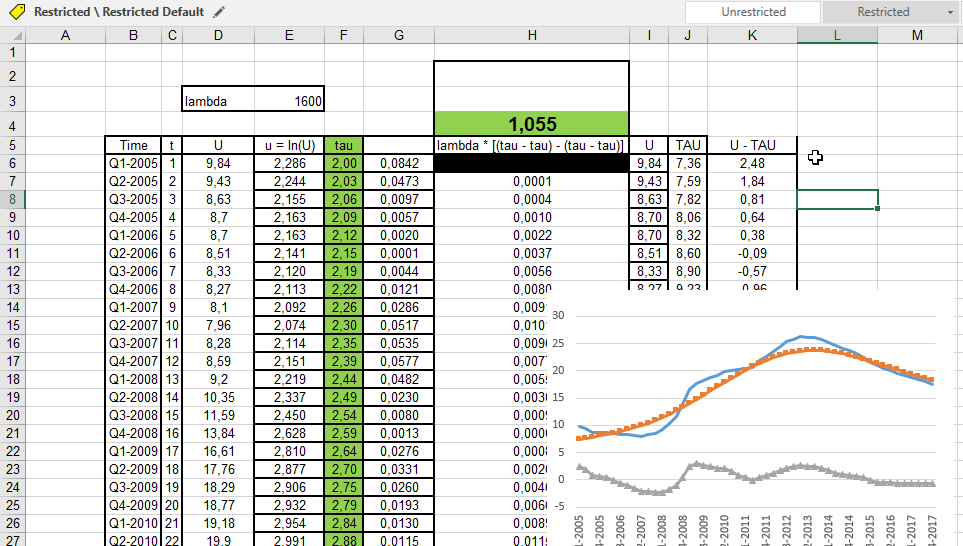

Nevertheless, I tackled my particular problem now the other way around. Instead of building the Hodrick-Prescott filter myself (with the help of the grg nonlinear solving method of the infamous excel solver), I looked for a ready-built package. Though I usually refrain from using scripting within KNIME, as I value the ease of low coding solutions, I found a python package, which provides the HP filter.

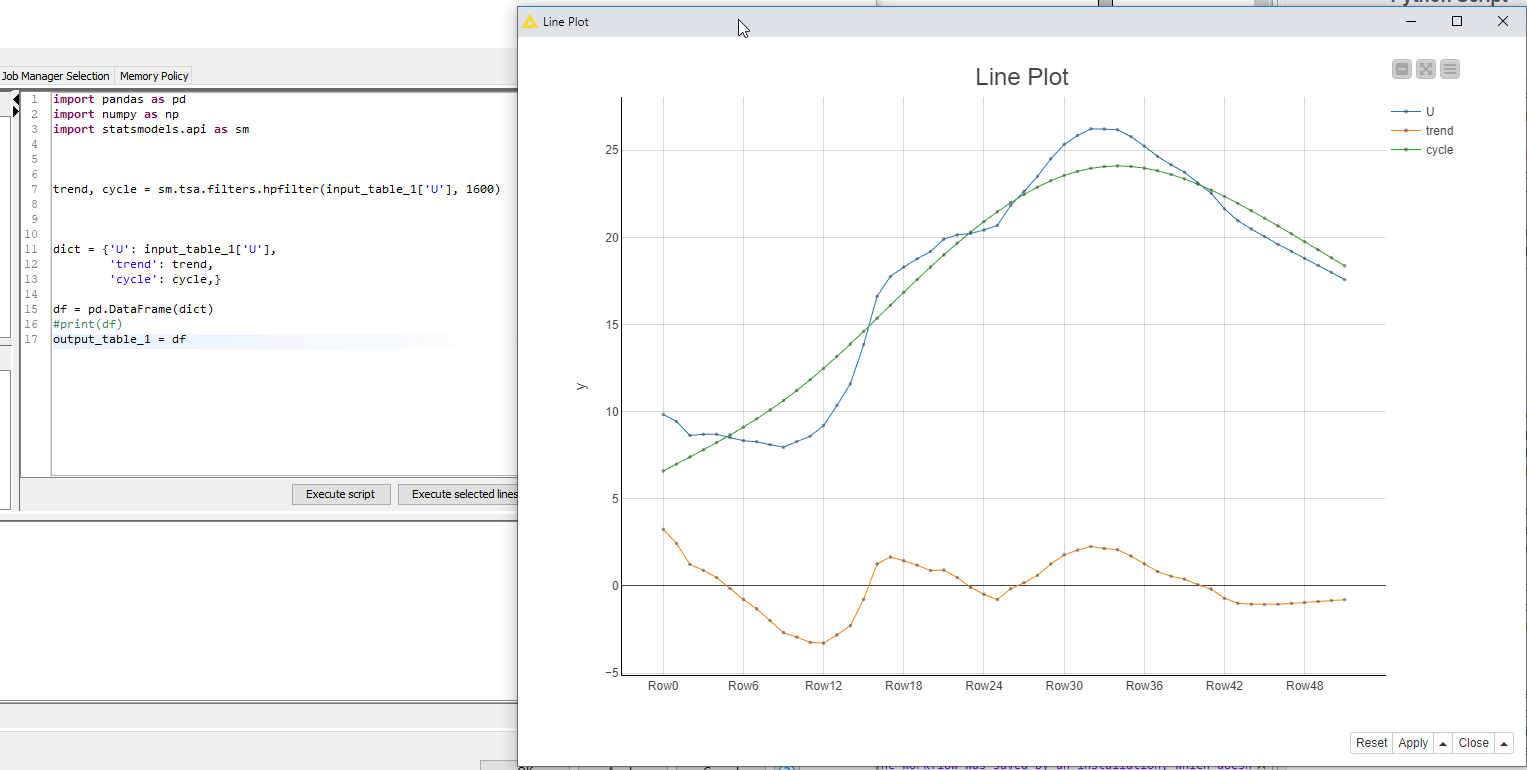

For the case someone is interested in the HP Filter solution in Python/KNIME, find screenprinted the solution, where U is the macroeconomic key figure, which I want to detrend.