Carsten,

Thank you for reaching out!

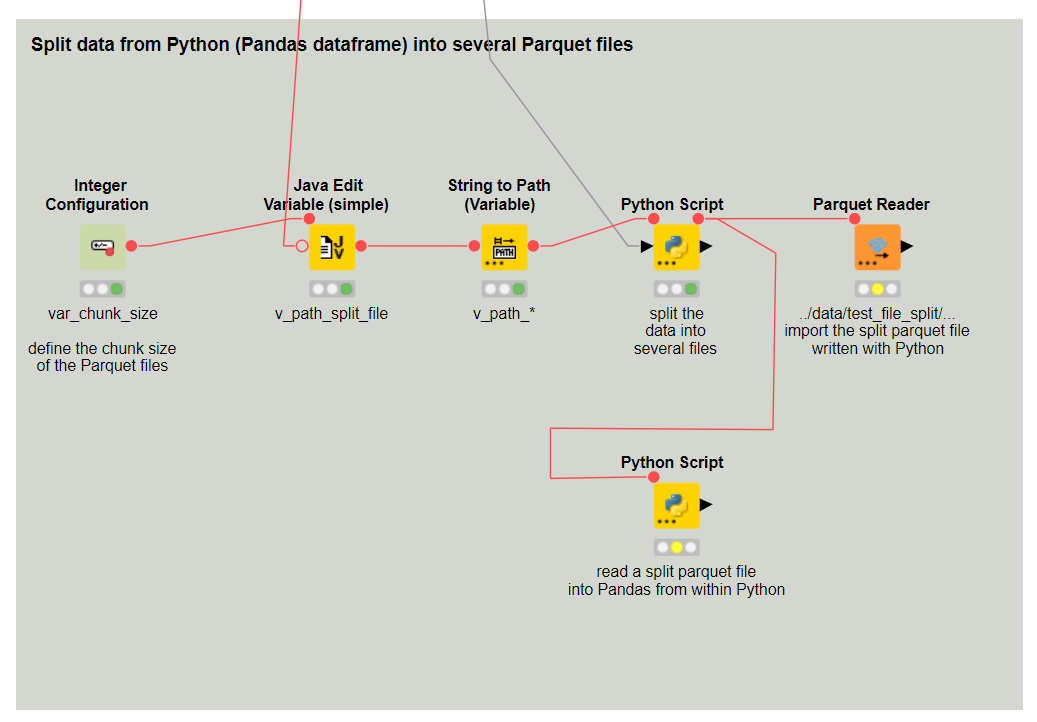

Thrilled to hear you are working on this for 5.3 When is that due to be out?

Also…splitting the file does not feel like a great option anyway.

I am using pandas.

…here is the script:

“”"

This script will merge the results of a random list of series with the client transaction file.

Provide an input of the transaction file from the client, the list of series you would like to use

The script will access FRED, calculate change metrics, then merge the results into the transaction file, and then return the merged results back into the workflow.

After this merge, you will have to re-map these results to the output mask.

INSTRUCTIONS

- Supply the FRED Series names and plain-english names in the dict_series_list using a dictionary format

- Run the script

- Remember to assign the newly merged series to the output mask.

“”"

#Clear memory for script run

globals().clear()

Import requisite libraries

import pandas as pd

import numpy as np

import pyfredapi as pf

import os

import datetime

import time

Set runmode (1-Development in Spyder , 0 - Production KNIME)

runmode = 1

EXECUTION PARAMETERS

dict_series_list = {‘CPIRECSL’:‘CPI - Recreation’,

‘PCUATRNWRATRNWR’:‘PPI - Transp. & Warehousing’,

‘FEDFUNDS’:‘Federal Funds Effective Rate’,

‘USACPALTT01CTGYM’:‘CPI-ALL’,

‘wpu80’:‘Construction (Partial)’,

‘HOUST1F’:‘New Private Housing’,

‘RHEACBW027SBOG’:‘Real Estate Loans: Residential Real Estate Loans: Revolving Home Equity Loans, All Commercial Banks’

}

#input_path = “x”

input_path = “x”

#output_path = x"

output_path = “x”

Pull in transaction data file, import matplotlib if running in DEVELOPMENT mode

if runmode==1:

pd.set_option(‘display.max_columns’, None) # See all columns in pd dataFrame

pd.set_option(‘display.max_colwidth’, 20) # Limit column width in pd dataFrame

pd.set_option(‘display.expand_frame_repr’, False) # Remove truncated outputs

st_df = pd.read_csv(input_path+“InitialAssembly100_PCT.csv”, nrows=10000)

#st_df = pd.read_csv(input_path+“InitialAssembly100_PCT.csv”, nrows=10000)

import matplotlib.pyplot as plt

else:

import knime.scripting.io as knio # Imports KNIME libraries when in the KNIME environment

st_df = knio.input_tables[0].to_pandas()

Set FRED_API_KEY as an environmental variable

os.environ[‘FRED_API_KEY’] = ‘1c6a58b07dfeb3b40c85c4de15d4a84d’

Create a dictionary to store dataframes for each item

item_series_dfs = {}

def get_series(item):

#Pull series information and store it as a pandas dataframe

Series_df = pd.DataFrame(pf.get_series(series_id=item))

# Keep the date and value fields

Series_df = Series_df.iloc[:,-2:]

Series_df[item+'Series'] = item

Series_df[item+'SeriesName'] = dict_series_list[item]

# Format the date and extract Year/Month fields for merge with transaction data

Series_df['date'] = pd.to_datetime(Series_df['date'])

Series_df['Month'] = Series_df['date'].dt.month

Series_df['Year'] = Series_df['date'].dt.year

Series_df[item+'value'] = Series_df['value']

# Calculate 3-month and 12-month rolling averages

Series_df[item+'3MRoll'] = Series_df[item+'value'].rolling(window=3).mean()

Series_df[item+'12MRoll'] = Series_df[item+'value'].rolling(window=12).mean()

# Shift data by 1 unit of previous period

df_prev1 = Series_df.shift(12) # Look back 12 month

df_prev3 = Series_df.shift(12) # Look back 12 months

df_prev12 = Series_df.shift(12) # Look back 12 months

# Calculate rolling averages for previous year

Series_df[item+'1M_prev'] = df_prev1[item+'value'] # Take the value from 1 month ago

Series_df[item+'3MRoll_prev'] = df_prev3[item+'value'].rolling(window=3).mean() # Take the mean value of the last 3 months from 3 months ago

Series_df[item+'12MRoll_prev'] = df_prev12[item+'value'].rolling(window=12).mean() # Take the mean value of the last 12 months from 12 months ago

# Calculate percent change in rolling averages

Series_df[item+'1M_CHG_PERC'] = (Series_df[item+'value'] - Series_df[item+'1M_prev'] ) / Series_df[item+'1M_prev'] # 1 month % change relative to past 1 month

Series_df[item+'3MRoll_CHG_PERC'] = (Series_df[item+'3MRoll'] - Series_df[item+'3MRoll_prev']) / Series_df[item+'3MRoll_prev'] # 3 months % change relative to past 3 months

Series_df[item+'12MRoll_CHG_PERC'] = (Series_df[item+'12MRoll'] - Series_df[item+'12MRoll_prev']) / Series_df[item+'12MRoll_prev'] # 12 months % change relative to past 12 months

if runmode==1:

# Plot the time series

plt.figure(figsize=(12, 6))

plt.plot(Series_df['date'], Series_df[item+'1M_CHG_PERC'], label='1 Month % Change')

plt.plot(Series_df['date'], Series_df[item+'3MRoll_CHG_PERC'], label='3 Month Rolling Average % Change')

plt.plot(Series_df['date'], Series_df[item+'12MRoll_CHG_PERC'], label='12 Month Rolling Average % Change')

plt.xlabel('Date')

plt.ylabel('Percent Change')

plt.title('Percent Change in Rolling Averages'+Series_df[item+'Series'].iloc[1,])

plt.legend()

plt.grid(True)

plt.xticks(rotation=45)

plt.tight_layout()

plt.show()

# Store the dataframe in the dictionary

item_series_dfs[item + '_df'] = Series_df

return pd.DataFrame(Series_df)

Create an empty dataframe for the results from FRED

fredresults_df = pd.DataFrame()

Create a WIDE format result with FRED Series information, this also will become teh source for item_series_dfs which is a dictionary of dataframes (item_series_dfs)

fredresults_df = pd.concat([get_series(item) for item in dict_series_list], ignore_index=True)

RETURN a dict of dataFRAMES we can process and merge seperately

Sort the dictionary by row count in descending order

sorted_dfs = sorted(item_series_dfs.items(), key=lambda x: len(x[1]), reverse=True)

Initialize the merged dataframe with the first dataframe

merged_df = sorted_dfs[0][1]

Left join the remaining dataframes in sorted order with explicit suffixes

for i, (, df) in enumerate(sorted_dfs[1:], start=2):

suffix = f’{i}’

merged_df = pd.merge(merged_df, df, on=[‘Year’, ‘Month’], how=‘left’, suffixes=(‘’, suffix))

Drop duplicate rows based on ‘Year’ and ‘Month’, keeping the earliest ‘date’ value

merged_df = merged_df.sort_values(‘date’).drop_duplicates(subset=[‘Year’, ‘Month’], keep=‘first’)

Reset the index

merged_df.reset_index(drop=True, inplace=True)

Identify and rename duplicate columns in merged_df

merged_df = merged_df.loc[:,~merged_df.columns.duplicated()]

Identify and rename duplicate columns in merged_df

merged_df = merged_df.loc[:,~merged_df.columns.duplicated()]

Drop columns starting with ‘date’ and ‘value’

merged_df = merged_df.loc[:,~merged_df.columns.str.startswith(‘date’)]

fredresults_df = merged_df.loc[:,~merged_df.columns.str.startswith(‘value’)]

Display the final dataframe

if runmode==1:

print(fredresults_df)

Merge the Series data to the transaction data

Left join st_df to fredresults_df on ‘Year’ and ‘Month’

st_df = st_df.merge(fredresults_df, on=[‘Year’, ‘Month’], how=‘left’)

Display the result

print(st_df)

Push the table out to KNIME

if runmode==1:

print(fredresults_df.columns)

# Create a DataFrame with just the column headings and data types

column_info = pd.DataFrame({

‘Column’: fredresults_df.columns,

‘Data Type’: fredresults_df.dtypes

})

# Write the DataFrame to a CSV file

column_info.to_csv(output_path+'fredresults_column_info.csv', index=False)

st_df.to_csv(input_path+"InitialAssembly100_PCT_FREDSeriesInc.csv", index=False)

else:

knio.output_tables[0] = knio.Table.from_pandas(st_df)